feature

Extreme money makeover

Published Thursday, 03-Feb-2005 in issue 893

This week the Gay & Lesbian Times presents “Extreme money makeovers.” As the New Year is well underway, many have made “better money management” a top priority on their lists of New Year’s resolutions. Easier said then done, isn’t it? To assist our readers, we have taken two profiles: a middle-aged lesbian couple with four children and a 30-year-old single gay male, and with the help of the Bair Financial Group, the Gay & Lesbian Times has laid out an extensive financial plan to assist them in attaining their goals. Perhaps you can learn from these examples. Take a look …

Family focuses on the future

Elise Brown and Lisa DeMarco had no idea where their friendship would take them when they met seven years ago. Elise married her boyfriend just out of college in 1988 and Lisa married as well in 1985. Elise and Lisa met in 1998. Their families grew close and did a lot of activities together. Elise has two daughters ages 8 and 13, and Lisa also has two daughters ages 13 and 17.

In November 2001 Elise and Lisa realized that their friendship was much more than just a typical friendship, and knew they wanted to spend the rest of their lives together. Soon after this realization, they divorced their husbands, moved in together, and have now been together for three years.

They both had been stay-at-home moms for six years and left without any assets or jobs lined up. Family Matters, San Diego’s GLBT parenting association, has been able to lend them support for their family.

They have done a tremendous job in starting over, and they are now ready to start focusing on their future.

Elise had a background in the package delivery business and was able to step back into this business world fairly quickly. Lisa used to work in the technology side of graphic design, but has been removed for some time. Therefore, it took Lisa a bit longer to get reestablished.

Goals

Elise and Lisa have four daughters they want to put through college. In addition, they would like to put more energy into their company, Girls N Sports, that they founded in 1999, as well as securing their retirement.

Recommendations

Emergency reserves: Elise and Lisa have been living on the edge as far as an emergency account. This account is the first bucket you can tap into if things go wrong (i.e., get laid off, have an extended illness, need to care for an aging parent, have a major car or home repair). Ideally we recommend having savings equal to at least three to six months of your expenses. In order to determine the amount, you need to have a clear picture on what your income is and what your expenses are. If you have a home equity line of credit, you could count on some of that for this reserve account, but remember it is still better to receive interest than pay interest.

For Elise and Lisa we determined they should have at least $20,000 in this type of account. Until you review your financial position and your expenses, you have no way of knowing where you may be able to cut some expenses or if you are deficient in some of the following areas.

Protection planning

Health insurance: Both families are very active in sports. Good health insurance is mandatory to protect the family from devastating medical bills. Both Elise and Lisa are sufficiently covered.

Survivor income needs: Since Elise and Lisa are dependent on each other’s income to pay their monthly expenses, and they have young daughters that they need to provide for should something happen to either one of them, we analyzed their need for life insurance.

Elise has a $50,000 life insurance policy that her work provides for her. Lisa is the beneficiary. Lisa has no life insurance at this time. Elise also is the beneficiary of two life insurance policies that her ex-husband owns. The death benefit would be used to continue child support payments.

In determining the minimum amount of life insurance a person would need, a rule of thumb is at least 10 times your annual salary and then add to that any other additional debt you would like paid off or expenses to be paid, such as college costs for the kids.

In Elise and Lisa’s case, they need a policy providing around $1, 231,600 on Elise and $1,486,000 on Lisa. This would provide enough capital to pay off the mortgage, the college funds and provide additional income for the other partner. If you have additional investments that you could liquidate, then you could use those funds to offset the life insurance need.

Fact: If you make the minimum payment on a $4,800 balance (average balance of U.S. cardholders) at the average annual 17-percent interest rate, it would take you 39 years and seven months to pay off that debt. You would pay $10,818.63 in interest alone, and a total of $15,619 for the privilege of charging the $4,800! Homeowners and auto insurance: Because of the involvement that Elise and Lisa have in the other business, and as a general rule, we recommend that they secure an umbrella liability policy to give them additional protection from an unforeseen accident or issue that may not be covered under their existing policy. Be sure to review with your property and casualty insurance agent that your coverage is current and sufficient. Many people were caught severely under-insured when we had the firestorm two years ago. You may be able to lower your premium by increasing your deductible and freeing up some more cash for your other goals.

Investment planning

At this time, Elise and Lisa have been focusing on staying afloat, but they will soon be in a position where they will be able to invest in their goals. Diversification is the key to investing, as well as targeting the right type of account for the time frame of when the funds will need to be used. Right now paying for college is their biggest concern.

College planning: The cost in today’s dollars for college at San Diego State without room and board would be about $4,500 a year for each child for a total of $100,000. Indexed for inflation and room and board, the cost could total approximately $285,000. If they were to provide for the total cost of college for all of the girls for four years, they would need to begin saving around $800 a month in an account earning 6 percent; the majority of that being for the oldest daughter since she is less than a year away from college. There may be funds that come from the children’s fathers, but Elise and Lisa do not want to count on it. A great place to save for college can be in a 529 College Savings Plan. The funds grow tax-free if used for college and you can change the beneficiary if the child does not need the funds.

Income tax planning: Since Elise and Lisa are domestic partners and not legally married, they must file separate tax returns. There are many ways that an accountant can advise clients on how to do effective tax planning. It is important that you go to the same tax professional who can prepare your taxes knowing both of your situations. Because Elise and Lisa own several businesses, they can take advantage of deducting certain expenses. In addition, they can set up special retirement plans.

Retirement: Both Elise and Lisa want to be able to retire at Elise’s age 65 and they would like to plan on a life expectancy of age 90. They want to factor current lifestyle expenses and that the house would be paid off. In this case, they would need to accumulate a little over $1 million. In order to reach this goal in 24 years, they will need to save about $1,000 a month with an 8.5 percent rate of return. The best place to begin saving is in their 401(k) accounts at work. Elise is now eligible and Lisa will be eligible in one year. The money contributed to this type of company plan is put in before taxes, so you pay less income tax now while your contribution grows tax-deferred for retirement. An additional investment vehicle is a Roth IRA. This is a unique account that allows you to invest up to $3,000 a year (an additional $500 if you are over age 50), and these funds grow tax-free. You can invest in this account in many different ways based on your tolerance for risk and your time frame for needing the money. There are restrictions to these funds that you will need to know before you set up this type of an account. It is important that you meet with an investment professional to determine your tolerance for risk. They can help you allocate these funds for maximum growth.

Estate planning

Estate planning for gay and lesbian couples can be challenging if you have not prepared the appropriate documents ahead of time. Basically, estate planning is making sure that all of your possessions go the person you intend them to go to when you die. In addition, with the proper documents, you can name whom you would like to make financial decisions for you through powers of attorney, as well as medical decisions if you are not able to through health care directives. In addition, since you have minor children, we need make sure that you each have named guardians for the children should either of you or their fathers pass away.

If you do nothing, the state will decide who gets your assets. If you do not have a will or a trust naming your partner as a beneficiary, she or he will not receive any of your assets.

Gay and on getting on track

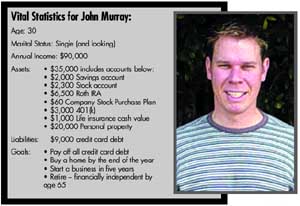

John Murray, an educated 30-year-old gay man, is participating in the Gay & Lesbian Times money makeover to make sure he is on track to securing his future. He said he had fun in his 20s and now it is time to get serious about his future.

John grew up in Yucaipa, a little town one and a half hours north of San Diego, and has led an interesting life. After joining the army and graduating from California State, San Bernardino, he worked in several jobs. After being laid off from a company that downsized, he moved to Hawaii to experience life there. He recently came back to San Diego, and seven months ago started working as an outside salesperson for a large home appliance and retail company. He has a large territory and travels most of his day to meet with homeowners.

Goals

John’s main goals are to pay off his credit card debt that he racked up while living in Hawaii, buy a house by the end of the year, start a business within five years and retire financially independent by age 65.

John is to be commended for taking control of his finances at his age. Unfortunately he accumulated a substantial amount of debt while he was living in Hawaii, but he quickly realized the impact the cost of this debt was having on him financially and got serious about aggressively paying it off. John did seek out the lowest interest credit cards he could get. This low-interest rate, combined with making extra payments, should enable him to be debt-free within three months.

Fact: If you make the minimum payment on a $4,800 balance (average balance of U.S. cardholders) at the average annual 17-percent interest rate, it would take you 39 years and seven months to pay off that debt. You would pay $10,818.63 in interest alone, and a total of $15,619 for the privilege of charging the $4,800! If you bought a couch with this credit card purchase, how do you think it would look in 39 years? Even worse, if you don’t have the couch any more, you are still paying for something you don’t even have!

John also has a goal of buying a house by the end of the year. Ideally, he should put at least 20 percent down so that he does not have to pay PMI (private mortgage insurance) – this is an insurance that you are forced to pay by the mortgage company if you have less than 20 percent equity in your home to protect them in case you default on your loan. There are so many loan options available to you today that you can tailor the loan to fit how long you think you will be in the home. Home prices in San Diego are at staggering prices, but a good agent and mortgage broker may be able to help you realize this dream.

John also wants to buy a business in five years. He is researching options of different opportunities that would allow him to own a low maintenance business that also would not take a lot of capital to start or a lot of employees to manage. Owning a business is often a great way to be able to accumulate additional wealth and allow you to have deductible taxable expenses that you would not otherwise have as an employee. We recommend that John thoroughly research the business ideas that he has and seek the advice of a qualified business coach that can help him write a business plan and help him launch and manage the business.

Recommendations

Emergency fund: John has done a good job in aggressively paying down his debt. Once debt-free he can begin to focus on building up his emergency fund to about $20,000.

Protection planning

Health insurance: John is covered through his employer for health and dental insurance. He pays a nominal amount each month.

Survivor income needs: John does not have anyone at this time depending on his income. He does own a whole life insurance policy that he bought last year having a death benefit of $25,000 and cash value of around $1,000. Currently the beneficiaries are his parents. This can be changed, if he chooses, once he has a partner that may depend on his income, or if they own property together with a mortgage or other debt they both incur.

Disability needs: As a single person this is a huge gap in his protection. If he is not able to work due to an accident or illness, he has nobody else’s income to fall back on. He should cover this risk with a disability insurance policy. His company may offer this type of coverage. If they do not, he should secure this coverage on his own.

Homeowners and auto insurance: Even though John does not own a house yet, he should still cover renter’s insurance and at some point in the near future look into securing an umbrella liability policy that will protect him above his normal policy limits.

Investment planning

It is great that John has seeded several investment accounts that he can contribute to as he has more cash flow. He is currently contributing to a Roth IRA that he will begin to be phased out of being able to contribute to when his income reaches $95,000, at which time he will want to concentrate even more on contributing the maximum to his 401(k) and his other investment account.

Income tax planning: John has very little in the way of tax deductions. Once he purchases his home, this will dramatically affect his income taxes. In addition, he needs to increase the amount he is contributing to his 401(k). This will also lower his taxable income.

Retirement: Even though John is only 30, he is thinking about how he can secure his retirement. The great thing about starting early is that he has time on his side. If John stays at his current pace of contributing 10 percent of his income to his 401(k) from now until retirement, he will retire at age 60 with over $1,000,000 in his 401(k) and reach his goal. In addition, he will have funds in his Roth IRA account as well as his other investment account.

Estate planning

John is currently single, so it is important that he still think about how he would want his estate distributed should something happen to him. Remember, the state decides if you do not have a will or trust naming who should get your assets. John also needs to name a person to be able to make financial and health decisions if he is not able to.

Financial planners’ biographies

Marci Bair, CFP, CSA is the president of the Bair Financial Group, an office of MetLife. Jenny Flynn, CSA is also a financial planner with the Bair Financial Group. They have two offices, one in Hillcrest and the other in Mission Valley. The duo prepares money makeovers and consult on a variety of financial planning topics for individuals, couples and business owners.

Bair is the president of Family Matters, San Diego’s GLBT parenting organization, one of the largest of its kind with over 1,500 members.

Flynn is on the board of directors at The Center and is involved with Film Out and Soroptimist International. Bair and Flynn are also available to provide a seminar for your company or organization on topics ranging from financial planning basics to charitable giving and estate planning. A plan similar to those presented above cost roughly $1,500. You may contact Bair Financial Group at (619) 497-2279.

|

|

Copyright © 2003-2026 Uptown Publications